Only two options reliably stop a power of sale in Ontario: sell the property, or remortgage it. Both work because they raise the full amount the lender is owed from the property's own equity, so they don't depend on the lender's goodwill. And in both cases the costs are paid out of the sale or mortgage proceeds, which means you generally need little or no cash up front.

Everything else you will read about (negotiating with the lender, fighting the sale in court, bankruptcy) either depends on the lender choosing to cooperate, depends on the lender having made a legal mistake, or simply does not stop a power of sale at all. This guide covers the two options that work, the situational options and their real limits, the exact deadlines set by Ontario's Mortgages Act (R.S.O. 1990, c. M.40), and what each path costs.

Can You Stop a Power of Sale in Ontario?

Yes — a power of sale can be stopped at any time before the lender's sale becomes firm, meaning before the lender accepts a binding agreement of purchase and sale with a buyer. You remain the legal owner throughout the process, and Ontario law builds in mandatory waiting periods that give you time to act. Watch the deadline carefully, though: the point of no return is the moment the lender signs a binding deal with its buyer, not the later closing date. Once the lender has listed the property and offers are in play, treat every day as your last and get legal advice immediately. The real question is which method you can actually count on:

| Option | Will it stop the power of sale? | What it depends on |

|---|---|---|

| Remortgage the property | Yes, reliable | Equity in the home. Costs come out of the new mortgage advance, not your pocket. |

| Sell the property yourself | Yes, reliable | Equity in the home. Costs come out of the sale proceeds on closing. |

| Pay the arrears (reinstate) | Yes, if you have the cash | A lump sum most borrowers in power of sale don't have. When it happens, the money usually comes from a remortgage anyway. |

| Negotiate with the lender | Sometimes | The lender's goodwill. They have no obligation to agree to anything. |

| Fight it in court | Rarely | The lender having made a legal mistake you can challenge, such as a defective notice or a premature step. |

| Bankruptcy / consumer proposal | No | Nothing. A mortgage is a secured debt, and insolvency does not stop a secured lender from enforcing against the property. |

The rest of this guide works through that table in detail, starting with the two reliable options. If you take one message from this page, make it this: plan around selling or remortgaging, and treat everything else as a bonus if it happens to work.

What to Do the Day the Notice of Sale Arrives

The single most expensive mistake homeowners make is doing nothing for the first two or three weeks. The 35-day redemption period is long enough to arrange a remortgage or a sale, but only if the work starts immediately. Here is the day-one sequence:

- Read the notice and diarize the dates. The Notice of Sale Under Mortgage states the amounts claimed (principal, interest, costs) and the date before which payment must be made. That date is your deadline for the protected window; write it down, and count backwards.

- Demand a section 22 statement in writing. Send the lender's lawyer a written request for a statement of the arrears and enforcement expenses. They must respond within 15 days, and it fixes the exact payout figure your remortgage or sale needs to clear.

- Check the notice for defects. Was it served on you and on everyone with a registered interest? Had your default actually continued 15 days before it was issued? Are the figures consistent with your records? Defects don't erase the debt, but a defective notice may have to be re-issued, and every re-issued notice restarts the 35-day clock.

- Pull your numbers together in one sitting. Current mortgage balance, arrears, a realistic value for the home (recent neighbourhood sales, or a quick agent opinion), and every other registered debt. Your equity, meaning the value minus everything owed, determines whether the two reliable options are open to you.

- Call a mortgage broker who handles power of sale files, the same week. Private and B-lender remortgages routinely fund in days to a few weeks from application. Starting the file in week one of the redemption period is comfortable; starting in week four is a crisis.

- Talk to a real estate lawyer before signing anything. A one-hour consultation to verify the lender's figures, review the notice, and confirm your deadlines is the best few hundred dollars you can spend in this process.

- Do not move out, and do not ignore mail. Leaving the property signals abandonment and removes any practical leverage; unopened envelopes contain the deadlines you are now living by.

If money is short, prioritize in this order: property insurance stays current (an uninsured default is a second, separate default), then the section 22 statement request, then professional advice. Everything else in this guide flows from knowing your exact numbers early.

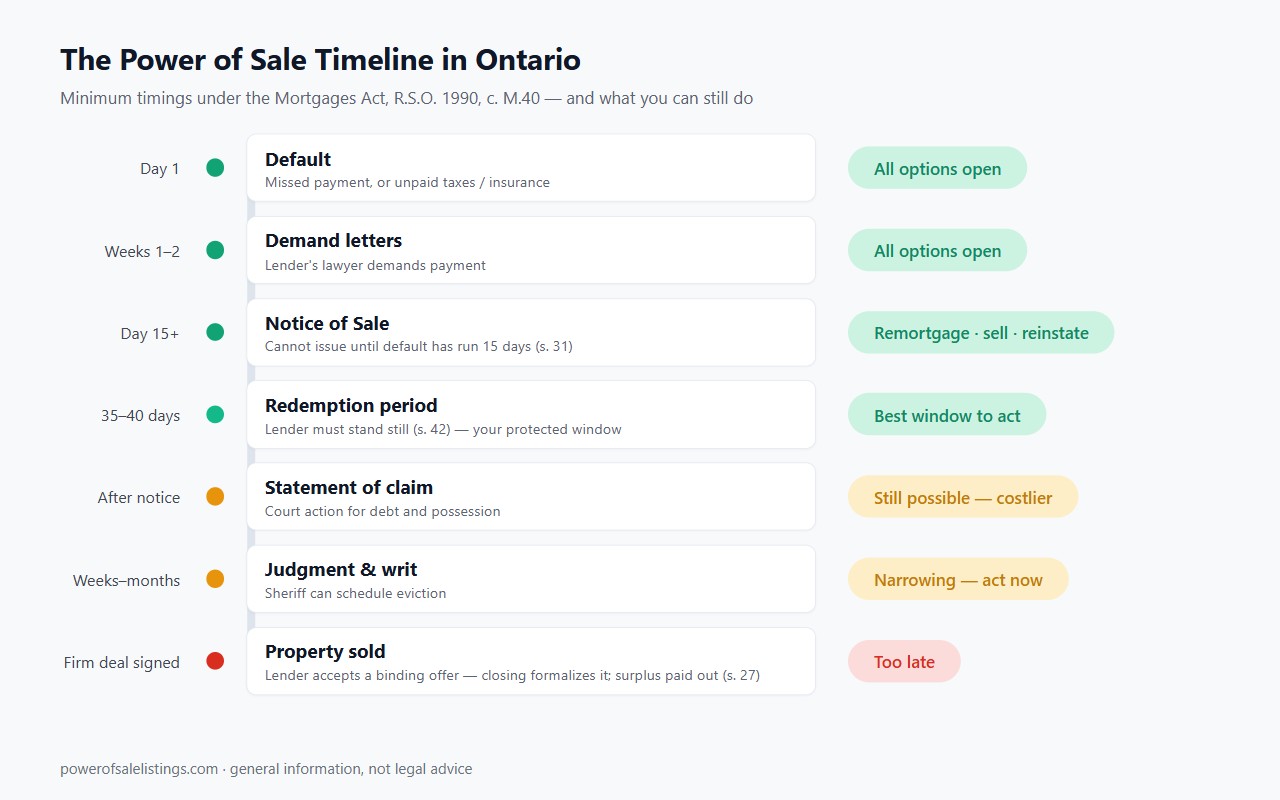

How the Power of Sale Process Works in Ontario

Power of sale is the remedy Ontario lenders use in the overwhelming majority of mortgage defaults because it is faster and cheaper for them than foreclosure. Almost every Ontario mortgage contains a contractual power of sale clause, which is governed by Part III of the Mortgages Act. The process follows a predictable sequence with legally mandated minimum timelines:

| Stage | Minimum timing | What you can still do |

|---|---|---|

| 1. Default: you miss a payment (or breach another term, such as not paying property taxes or insurance) | Day 1 | Everything. Call the lender, catch up the payment, or start a remortgage before enforcement costs begin to stack up. |

| 2. Demand letters: the lender (or its lawyer) demands payment | Usually within the first weeks of default | Pay the arrears, or start the remortgage or sale. Enforcement legal costs are still small at this stage. |

| 3. Notice of Sale Under Mortgage: the formal statutory notice served on you and everyone with an interest in the property | Cannot be issued until the default has continued for at least 15 days (s. 31) | Remortgage, list the property, reinstate under s. 22, or negotiate. The redemption period now starts. |

| 4. Redemption period: a mandatory standstill | At least 35 days after the notice is given (ss. 31–32); commonly 40 days where the property is a matrimonial home occupied by a married couple | This is your protected window. Section 42 bars the lender from taking any further step (no statement of claim, no possession, no listing agreement) until the notice period expires. A premature step can invalidate the notice. |

| 5. Statement of claim: after the notice expires, the lender typically sues for the debt and possession | After the 35-day period ends | You can still remortgage, sell, reinstate, or redeem. Filing a statement of defence buys time if you have a genuine dispute. |

| 6. Judgment and writ of possession: the court orders possession; the sheriff can schedule an eviction | Weeks to months later, depending on the court | Options are narrowing and costs are high, but the sale still has not happened. A completed remortgage or sale can still stop it. |

| 7. Sale of the property: the lender lists with a realtor and sells at market value | After possession (or with tenants/owners still in place) | Until the lender accepts a binding agreement of purchase and sale, redemption remains possible. Once that agreement is firm it is too late — the closing that follows only formalizes the transfer. If the property is listed, get legal advice the same day. |

If a mortgage somehow contains no power of sale clause, the lender can instead rely on the statutory power of sale in section 24, which requires a longer runway: three months of default and 45 days' notice. In practice you will almost always be dealing with the contractual version and its 15-day/35-day timeline.

Two features of the process matter enormously for your strategy:

- The lender must sell at market value. The lender has a duty to account for the proceeds and must not sell improvidently. It cannot dump the property for whatever clears its own debt.

- You keep the equity. Under section 27, sale proceeds go first to the costs of the sale, then to the mortgage debt, then to subsequent encumbrancers — and any surplus belongs to you. This is the single biggest difference from foreclosure.

Ontario Power of Sale Market Snapshot

Power of sale is more common than most homeowners realize. This site tracks every active power of sale listing in Ontario directly from MLS® sources, so the numbers below are our own live data rather than a third-party estimate. As of July 12, 2026:

| Ontario power of sale market | Right now |

|---|---|

| Active power of sale listings | 876 |

| New power of sale listings in the last 30 days | 243 |

| Municipalities with at least one active listing | 157 |

| Most active municipalities | Toronto (160) · Brampton (43) · Hamilton (29) · London (28) · New Tecumseth (26) |

You can verify every figure yourself: browse the active listings, see them on a map, or dig into the monthly market statistics. The reason this data belongs in a guide about stopping a power of sale: every listing above is a lender selling someone's home with enforcement costs stacked onto the debt and an "under power of sale" label that invites discounted offers. The goal of this guide is to keep your home off that list — or, if selling is the right answer, to have you sell on your own terms instead.

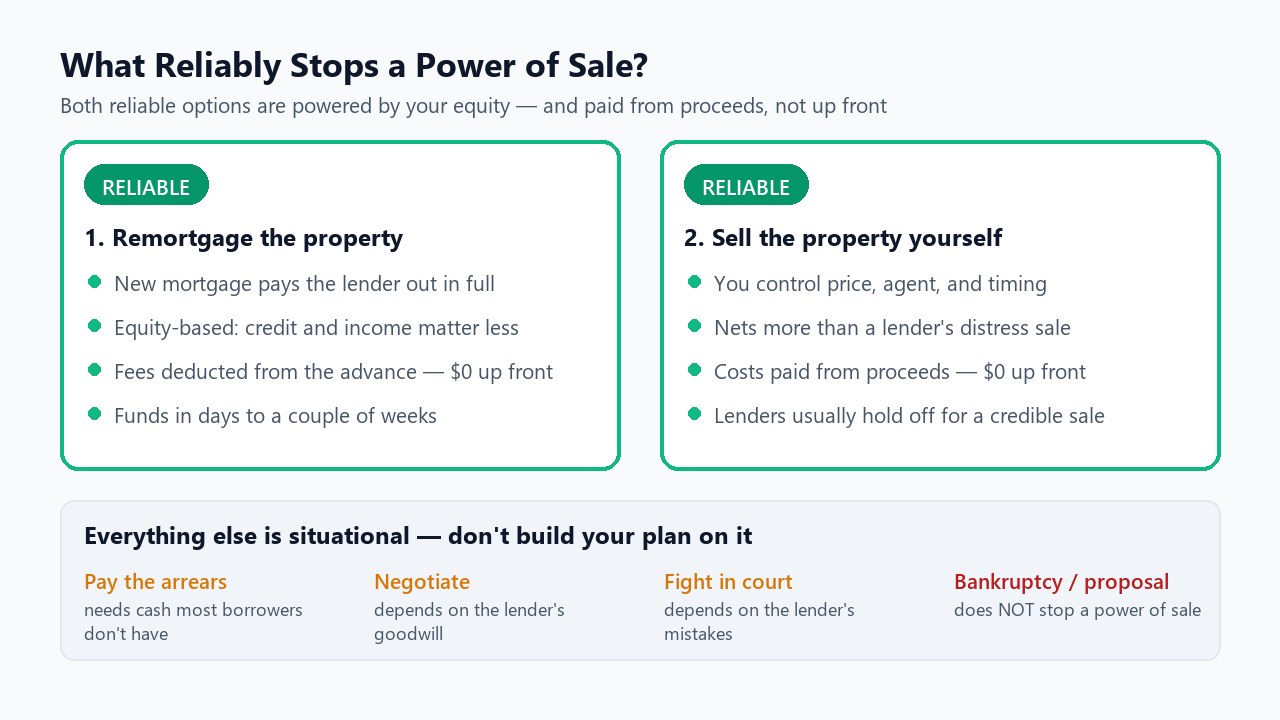

The Only 2 Options That Reliably Stop a Power of Sale

Selling and remortgaging share the three properties that make them dependable: they raise the entire payout the lender is owed, so the lender has no say in the matter; they are powered by your home's equity rather than your income or credit score; and their costs are paid out of the proceeds rather than out of your pocket. That last point gets skipped in most write-ups. People facing power of sale usually have a cash-flow problem rather than an equity problem, and these are the two options that still work when cash flow is broken.

Option 1: Remortgage the property

A new mortgage pays out the defaulting lender in full, including arrears, penalties, and enforcement costs, and the power of sale dies at funding. Banks rarely refinance a borrower already in power of sale, but that is not the end of the road: B-lenders and private lenders pay out powers of sale every week in Ontario, because they lend primarily against the equity in the home rather than your credit score or income documents.

- Speed: equity-based approvals commonly come within a day or two, and funding within days to a couple of weeks — comfortably inside the 35-day redemption period if you start promptly.

- Upfront cost: generally none. Lender fees, broker fees, and legal costs are deducted from the mortgage advance at closing.

- The trade-off: higher rates and fees than a bank mortgage, typically on a one- or two-year interest-only term. A private mortgage is a bridge, not a destination. The plan is to stop the sale, stabilize, repair your credit, and refinance back to a mainstream lender.

- Who it fits: homeowners with meaningful equity who want to keep the home, or who need time to sell on their own schedule instead of the lender's.

Option 2: Sell the property yourself

If keeping the property is not realistic, selling it yourself usually nets you more than letting the lender sell it. You control the listing price, the agent, the timing, and the presentation; you avoid months of accumulating enforcement costs and penalty interest; and you avoid the discount that comes with an "under power of sale" listing. This is not a contradiction of the lender's duty to sell at market value: that duty means not selling improvidently on the day of sale — it does not oblige the lender to stage the home, wait for the strongest buyer, or spare you the enforcement costs and penalty interest that accrue in the meantime, all of which come out of your equity first. The sale proceeds pay out the mortgage on closing and the power of sale ends.

- Upfront cost: generally none. Real estate commission, legal fees, and the mortgage payout all come out of the sale proceeds on closing day.

- Keeping the lender at bay: tell the lender's lawyer you are listing, provide the listing agreement and any offers, and most lenders will hold enforcement while a credible sale is in progress. If more time is needed, a short private mortgage can pay out the lender and buy you a calm, full-price sale.

- The evidence: browse the current power of sale listings and market statistics to see how lenders price and market these properties. A well-presented private sale of the same house usually does better.

Transparency note: remortgaging and selling — the two paths this guide recommends — are the services Jonathan and Mortgage Broker Store provide, so we have an interest in you choosing them. That is exactly why this guide cites the Mortgages Act sections, the regulators, and official resources throughout: verify everything independently, and spend an hour with a real estate lawyer before signing anything, including with us.

Need to stop a power of sale now? Jonathan Alphonso and the team at Mortgage Broker Store specialize in exactly these two paths: private and B-lender remortgages that pay out powers of sale, and managed sales that protect your equity. Call 416-499-2122 or email jonathan@mortgagebrokerstore.com for a free, no-obligation quote. You will get a same-day answer, and there is nothing to pay up front.

How Fast Can You Stop a Power of Sale?

With equity in the property, a power of sale can often be stopped within one to two weeks, sometimes within days. Equity-based private lenders can approve in 24–48 hours because the decision rests on the property, not on document-heavy underwriting; funding follows as soon as an appraisal and legal work complete. A reinstatement (paying the arrears) is even faster if the cash exists: certified funds delivered to the lender's lawyer stop the process the day they are received.

What that speed does not mean is that you can safely wait. Every week of delay adds enforcement costs to the payout figure, and past the redemption period a statement of claim adds thousands more. As a rule, a file started in week one of the 35-day window closes calmly; a file started in week four needs emergency treatment and pays emergency pricing.

The Other Options (and Why You Can't Rely on Them)

Each of the following can work in specific circumstances. None of them is a plan. They fall into three categories: options that need cash you probably don't have, options that depend on the lender's goodwill, and options that depend on the lender's mistakes.

Paying the arrears (reinstatement): works if you have the cash

Section 22 of the Mortgages Act gives you a real legal right: pay the missed payments plus the lender's enforcement costs (not the accelerated full balance) at any time before the property is sold or a court action begins, and the mortgage is reinstated. Lenders cannot contract out of it. The catch is practical rather than legal. A borrower who could produce several months of payments plus legal fees in a lump sum usually wouldn't be in power of sale in the first place. When reinstatement does happen, the money most often comes from a remortgage, a family loan, or the early proceeds of a sale, which brings you back to the two reliable options.

Paying out the mortgage in full: same story, bigger number

Redemption, meaning paying out the entire balance plus costs, stops the process cold at any stage before the lender's sale becomes firm. Almost nobody has the cash on hand; when redemption happens, a new mortgage or a sale is what funds it.

Negotiating with the lender: depends entirely on their goodwill

Forbearance agreements, payment deferrals, and capitalizing arrears onto the balance all exist, and institutional lenders have loss-mitigation departments that sometimes grant them. But everything on that list is a favour, not a right. The lender has no obligation to agree, private lenders usually won't, and negotiating does not pause the statutory clock unless a signed agreement says so. Negotiate in parallel with a real plan, never instead of one, and get anything agreed in writing.

Fighting it in court: depends on the lender's mistakes

A statement of defence can genuinely help when the lender got something wrong: the arrears figure is inflated, the notice of sale was defective or improperly served, the notice was issued before the default had run 15 days, or the lender took an enforcement step during the section 42 standstill (which can invalidate the notice entirely). That is why step 3 of the day-one checklist is to scrutinize the notice. But if the paperwork is clean, and lenders' lawyers do this every day, a defence with no arguable merit just adds the lender's court costs to the debt you must clear. Treat litigation as a way to buy time for a remortgage or sale, and only on a lawyer's advice.

Bankruptcy or a consumer proposal: will not stop a power of sale

Homeowners are routinely sold false hope here, so it is worth saying bluntly: neither bankruptcy nor a consumer proposal stops a power of sale. A mortgage is a secured debt. The insolvency stay of proceedings protects you from unsecured creditors (credit cards, tax debt, judgments), but a secured lender's right to enforce against its collateral continues. Filing does not cure the mortgage default, does not pay the arrears, and does not prevent the sale.

The only legitimate role insolvency plays is indirect: if unsecured debts are what broke your budget, a consumer proposal can cut those payments so you can afford the mortgage going forward, once the arrears are dealt with by other means. If someone pitches a proposal or bankruptcy as the way to "save your home" from a power of sale, get a second opinion from a Licensed Insolvency Trustee and a mortgage professional before signing anything.

How Much Time Do You Have?

At an absolute minimum, you have 50 days from default before a sale can occur: 15 days before a notice of sale can be issued, plus 35 days of redemption period after it is given. In practice the process takes considerably longer. Lenders typically send demands before issuing a notice, courts take weeks to months to issue judgment and a writ of possession, and the property must then be listed and sold.

A realistic timeline from first missed payment to a completed sale is four to eight months or more. But do not confuse the total length of the process with the length of your best options:

- Days 1–15 (before a notice can issue): maximum flexibility, minimum cost. A missed payment can often be fixed with a phone call and a payment.

- The 35-day redemption period: your legally protected window. The lender cannot take further steps (s. 42). This is when to arrange the remortgage or start the sale.

- After the notice expires: everything still works, but a statement of claim adds thousands in legal costs to the debt you must clear, and each subsequent stage adds more.

- Once the lender accepts a binding agreement of purchase and sale: nothing works. The sale is legally made at that moment — closing only formalizes it — and your rights are limited to the surplus proceeds.

Mark the dates on the notice of sale the day it arrives. The notice must state the amount claimed and the date before which it must be paid. Those numbers are the skeleton of your plan.

What It Costs to Stop a Power of Sale

The good news is that the two reliable options generally cost nothing up front. A remortgage deducts its lender fee, broker fee, and legal costs from the mortgage advance; a sale pays its commission and legal fees out of the proceeds on closing. That is what makes them workable for homeowners whose cash flow is already broken. What you are really paying is out of equity, and every week of delay shifts more of that equity to the lender's lawyers. Typical Ontario ranges:

| Cost | Typical range | Paid when |

|---|---|---|

| Mortgage arrears | Your missed payments + interest | The core amount; grows every payment date. |

| Lender's legal fees (notice of sale stage) | $2,500–$7,500+ | Added to the mortgage debt; cleared from your remortgage or sale proceeds. |

| Lender's legal fees (litigation/possession stage) | $10,000–$25,000+ | Also added to the debt, which is the strongest reason to act during the redemption period. |

| Remortgage costs (if you go that route) | Lender fee 1–3% + broker fee 1–2% + legal ~$1,500–$3,000 | Deducted from the mortgage advance at closing; no upfront cash. |

| Sale costs (if you sell) | Commission ~4–5% + legal ~$1,500–$2,500 | Paid from sale proceeds on closing; no upfront cash. |

| Your own lawyer (advice/defence) | $1,500–$5,000+ | One of the few real out-of-pocket costs; a one-hour consultation is far less. |

These are typical market ranges, not quotes; every file differs. What matters is the slope. A default cured in week two might cost a few hundred dollars in fees, while the same default cured after judgment can cost tens of thousands of dollars of equity. Speed is the cheapest thing you can buy.

Power of Sale vs Foreclosure in Ontario

The key difference: under a power of sale the lender only sells the property and must pay any surplus equity back to you; under a foreclosure the lender takes ownership of the property itself and your equity is gone. People use "foreclosure" loosely to mean any forced sale, but in Ontario law they are different remedies with very different consequences:

| Power of sale | Foreclosure | |

|---|---|---|

| Who ends up owning the property | A buyer on the open market; the lender only sells | The lender takes title to the property itself |

| What happens to your equity | Surplus after the debt and costs is paid back to you (s. 27) | Lost; the lender keeps the property regardless of its value |

| Can the lender sue for a shortfall? | Yes. If the sale doesn't cover the debt, you can be pursued for the deficiency | Generally no; taking the property extinguishes the debt |

| Court involvement | Minimal; notice-driven and fast | A full court proceeding; slow and expensive |

| Typical duration | Roughly 4–8 months | Often a year or more |

| How common in Ontario | The default remedy, used in the vast majority of cases | Rare; used mainly where there is little or no equity |

Because the lender must return your surplus under a power of sale, homeowners with equity have real leverage and real protection. That same equity is also exactly what powers the two reliable exits (remortgaging and selling), which is why the amount of equity in your home, more than your income or credit, determines how many ways out you have.

What Happens If You Don't Stop It

If no option is exercised, the lender completes the sale, and on closing your ownership ends. The proceeds are applied in the order set by section 27 of the Mortgages Act: costs of the sale first, then interest and principal on the mortgage, then subsequent registered claims (second mortgages, liens, executions), with any surplus paid to you. The lender must account for the sale, and if it sold carelessly below market value you can challenge the accounting. But litigation after the fact is a poor substitute for equity protected before the sale.

Three consequences deserve emphasis:

- Deficiency claims survive the sale. If the proceeds do not cover the debt and costs, the lender can sue you personally for the shortfall. Power of sale is not a clean break the way foreclosure is.

- Your credit takes a multi-year hit. The default, the enforcement, and any judgment are reported; expect mainstream borrowing to be difficult for several years.

- Eviction is real. After a writ of possession, the sheriff enforces it. Waiting for that stage sacrifices any control over your family's timing.

If the sale genuinely cannot be prevented, shift the goal from "keep the house" to "maximize the surplus": cooperate on access and showings (a hostile, unshowable house sells for less, and that loss is yours, not the lender's), verify every cost the lender claims, and have your own lawyer review the accounting before signing anything.

How to Avoid Power of Sale in the Future

The most reliable way to avoid a power of sale is to treat the very first missed payment as an emergency and contact your lender before enforcement begins. Every option in this guide is cheaper, faster, and more available before a Notice of Sale is issued than after. Once you have stopped a power of sale, make it the last one:

- Treat one missed payment as an emergency. The cheapest power of sale is the one that never starts. Call the lender before they call you; borrowers who reach out early get accommodations that late callers do not.

- Keep property taxes and insurance current. Both are defaults under standard mortgage terms even if payments are perfect, and unpaid taxes are a common trigger on private mortgages.

- If you used a private bridge, plan the exit from day one. Interest-only private payments are survivable; a private mortgage you cannot renew or refinance at maturity is how second powers of sale happen. Set the refinance-back-to-a-bank milestones (credit score, income documentation) the week the bridge closes.

- Watch your renewal dates. A renewal at sharply higher rates is the modern path into default. Start shopping 120 days before maturity, and involve a broker early if income or credit has weakened.

- Do not borrow against the home to pay unsecured debt without a budget fix. Consolidations that just reload credit cards convert survivable unsecured debt into a mortgage default risk.

Where to Get Help in Ontario

Power of sale files are won by assembling the right help quickly. These are the official resources every Ontario homeowner in this position should know:

- The statute itself: the Mortgages Act, R.S.O. 1990, c. M.40 on Ontario's e-Laws. Sections 22 (reinstatement), 24 (statutory power of sale), 31–32 (notice and redemption period), 42 (standstill during the notice period), and 27 (distribution of proceeds) are the ones cited throughout this guide.

- Finding a lawyer: the Law Society of Ontario's referral resources can connect you with a real estate or civil litigation lawyer, including options for a free initial consultation. If your income is limited, ask about legal clinics in your area.

- Checking a mortgage broker or agent's licence: anyone arranging a private mortgage for you must be licensed by the Financial Services Regulatory Authority of Ontario (FSRA). Verify the licence before paying any fee. Distressed homeowners are a favourite target of unlicensed "rescue" schemes.

- Mortgage-default help from the federal government: the Financial Consumer Agency of Canada's guidance on trouble paying your mortgage and CMHC's mortgage payment difficulties resources explain the relief programs federally regulated lenders offer.

- Insolvency advice: only a Licensed Insolvency Trustee (regulated by the federal Office of the Superintendent of Bankruptcy) can file a consumer proposal or bankruptcy. As covered above, treat any claim that insolvency will stop a power of sale as a red flag.

Be cautious with anyone who cold-calls or door-knocks after a notice of sale becomes public, promises to "save your home" for an upfront fee, or pressures you to sign a transfer of title. If a rescue plan involves you giving up ownership or signing documents you don't understand, walk it past a lawyer first. Under time pressure, bad actors count on you skipping that step.

About the Author

Jonathan Alphonso, MBA is the Principal Broker at Mortgage Broker Store (licensed mortgage broker, FSRA Lic. M08005247; brokerage licence #12800), with more than 15 years in private and alternative lending. He has spent those years helping Ontario homeowners understand and respond to the power of sale process, arranging the private mortgages and refinancing that pay powers of sale out, and writing plain-language guides drawn from real files so families can act early and protect their equity. He also builds and maintains this site's database of Ontario power of sale listings. You can verify his licence through the FSRA public registry. Read his full bio.

This guide is general information about Ontario law and mortgage practice, not legal or financial advice. Power of sale files move quickly and turn on their specific facts; speak with a real estate lawyer or licensed mortgage professional about your situation.

Get a Free Power of Sale Consultation

If you are facing a power of sale right now, the two options that reliably work (remortgaging and selling) both get harder and more expensive every week you wait. Jonathan and the Mortgage Broker Store team review power of sale files every day and will tell you plainly which path fits your equity, your timeline, and your goals:

- Call 416-499-2122 for a same-day answer

- Email jonathan@mortgagebrokerstore.com

- Request a free quote online (no obligation, nothing to pay up front)

Researching the market first? Our database tracks every active power of sale listing in Ontario (currently 876 properties) with photos, pricing, and history:

- Browse all active power of sale listings

- Search by map to see activity near you

- Market statistics: median prices and volumes by month

- New to the site? Start with how to use this site or the FAQ